India is one of the biggest consumers of coal globally. In 2024, India’s coal consumption grew 10% to a whopping 1245 Mt (million metric tonnes) with the power sector accounting for a bulk of that consumption. According to the Coal Ministry’s Year-End Review, the supply of coal to the power sector during the calendar year was approx 793 Mt, a growth of roughly 5% from the previous year, where consumption stood at approx 755 Mt.

It’s safe to say that in many ways, India runs on coal! And getting that coal to power plants and other industries is a mammoth task. In the previous article, we looked at some of the key aspects of coal transport in India. How much coal is transported, the different methods used to transport coal, how much it costs, and what the government plans to do to make it efficient and economical, with the Coal Logistics Policy. In this article, we’ll look at how the policy will affect key stakeholders.

The goals: Coal Logistics Policy and Plan

India’s power demand is rising rapidly and coal-fired power plants supply nearly 70% of the country’s electricity. Beyond the power sector, known as the regulated sector, industries like steel and cement—part of the non-regulated sector—are also expanding and require increasing amounts of coal.

To meet rising demand, coal production increased by 12.1% to 880.72 million tonnes as of February FY24, up from 785.39 million tonnes in FY23. According to the Policy, India’s coal consumption is projected to reach 1.5 billion tonnes by 2030, highlighting the need for efficient logistics.

Even though coal production is increasing, supply remains restricted due to logistics and transport challenges. Roadways are slower, while rail networks face heavy congestion at key junctions, making coal logistics a major bottleneck.

India’s Coal Logistics Policy and Plan 2024 aims to modernise and enhance the efficiency of coal transportation, emphasising a shift towards a railway-based system for first-mile connectivity (FMC) projects. (FMC refers to the movement of coal from the mine to the nearest railway sliding or despatch point.) The government plans to increase the share of Railways in coal transportation from the current 65% to 86% by 2030. The approach is to:

- Reduce the share of road transportation

- Increase the share of rail transportation

- Reduce overall logistics costs with network optimisation

- Reduce carbon emissions

This strategic move is expected to reduce rail logistics costs by up to 14%, resulting in annual savings of approximately 21,000 crore. The plan addresses the need to expand coal mining and scale up evacuation infrastructure (moving coal out of mines) as the demand for coal in electricity generation in India continues to grow. Given that railways and roadways transport a bulk of the coal in India, this policy is bound to impact both these sectors, as well as key players in the logistics and infrastructure space and other stakeholders. Here’s a look at how coal transport will affect logistics.

The impact: Railways

India’s coal reserves are primarily located in the eastern and central regions, with Odisha, Chhattisgarh, Jharkhand, and parts of Madhya Pradesh accounting for 75% of the country’s raw coal dispatches. But with the congestion of the railway network, dedicated coal transportation corridors are needed to ensure timely supply to power plants and industries.

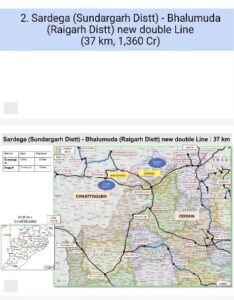

To meet this demand, the Ministry of Coal in late 2024 identified 38 priority rail projects under the coal logistics plan to enhance coal evacuation and transport. Of these, five projects have been commissioned and three are under construction. Two major approved projects are located in Odisha, spanning multiple coal blocks. These new rail lines aim to shorten the route between the Sardega and Talcher mines and the respective power plants they supply to in northern and western India, cutting transportation costs and speeding up coal deliveries.

The 37.24 km Sardega-Bhalumuda double line will streamline coal evacuation from the IB Valley and Mand-Raigarh Coalfields, supporting Mahanadi Coalfields Limited (MCL) and private mines, cutting transportation distances to power plants in Northern India. In the Talcher region, another key rail line is being developed to improve coal evacuation to the western regions of India.

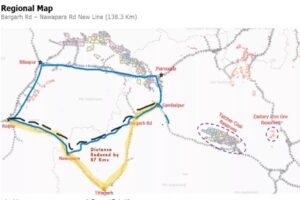

The 138.32 km Bargarh Road-Nawapara Road single line will improve coal transportation from the Talcher Coalfield, offering a more direct route to Nagpur and western regions.

Railway supply companies stand to benefit in a big way; to meet the demands of these proposed rail lines and the projected number of 86% coal evacuation by rail by 2030, the government needs an additional one lakh wagons. And rail logistics and manufacturing companies are already seeing the effects in their order books.

- Titagarh Rail: In March 2024, wagon manufacturer Titagarh Rail systems won an order worth INR 1900 crore from the Indian Railways, for the supply of 4463 freight wagons, used for the transport of bulk goods like coal and iron ore.

- Jupiter Wagons: Also in March 2024, Jupiter Wagons secured an order worth INR 957 crore from the Ministry of Railways, for the supply of 2237 BOSM wagons, used for coal and iron ore transport. BOSM stands for Boxn-HL (High-sided Open Wagon) with Side Mechanism.

- SAIL-RITES: In May 2024, SAIL-RITES, a joint venture between the Steel Authority of India Limited and Rail India Technical and Economic Service, was awarded a wagon contract worth INR 818 crore.

- Texmaco: In October 2024, Texmaco secured a contract worth INR 293 crores for 677 wagons, known as Bogie Open Rapid Discharge Hopper (BOBRN) wagons, designed for coal transportation.

And it’s not just these players, the strategic emphasis on rail infrastructure is also expected to benefit other railway companies involved in coal transport by increasing coal freight volumes.

The impact: Roadways

While railways stand to gain, roadways, which are the second biggest transporters of coal, will likely see a decline. Not just because of the Policy’s push to increase the share of rail transport, but also because of carbon emissions goals. Roadways have a much higher emission of 62 gCO₂/tonne-km (grams of carbon dioxide per tonne-kilometre), compared to rail at 22 gCO₂/tonne-km.

The use of trucks for long-distance coal movement will decrease, leading to lower demand for road logistics services for coal transport. However, according to the Ministry of Coal’s annual report 2023-24, there is a plan to develop roads for small-distance transport of coal to dispatch points, which may open up new opportunities for road transporters and infrastructure firms.

The impact: Other stakeholders

Since the policy’s main focus is on improving rail connectivity, infrastructure firms and entities that are involved in constructing and upgrading rail networks, loading and unloading facilities, and storage/warehousing stand to benefit as the railways enhance their infrastructure. Integrated logistics companies may also stand to gain, particularly those offering end-to-end and multimodal services, for a more effective coal evacuation system.

India’s Coal Logistics Policy and Plan 2024 has been designed to create a more efficient, cost-effective, and sustainable coal logistics framework, creating fresh opportunities for key stakeholders. So it’s worth keeping an eye on rail, logistics, and infrastructure firms, as these sectors work to cater to the Coal Ministry’s ambitious goals.

Sources

https://www.iea.org/reports/coal-2024/demand

https://energynews.pro/en/india-accelerates-38-rail-projects-to-improve-coal-transport/